How Do Startups and Insurance Connect?

For most businesses today, including startups, business insurance should be considered a mandatory requirement. It can be hard to know what insurance coverage you need when you're launching a business.

Law requires certain types of insurance, but other options can offer additional coverage, whether it’s for business associates, employees, or potential investors.

Ultimately, insurance, whether it’s for a small startup or a large corporation, is necessary to protect your employees and encourage investment in the business you have worked hard to create.

Insurance for emerging startups is essential and finding the right insurance types for your startup may seem daunting, but we are here to help.

Who Needs Startup Insurance?

Startups are temporary enterprises working to deliver new, innovative products or services in a variety of industries, from Art insurance to Technology insurance. Despite being enterprises, startups still need to be covered by insurance while they work towards developing scalable business models and becoming full-fledged companies. In times of crisis, a startup recovery plan is essential to get back on your feet. Whether you have been in the industry for a while or you are establishing your startup now, insurance is a top priority to help your business recover and keep you covered at all times.

Tailored insurance requirements for startups

Your insurance needs change as you increase your revenue, headcount, office space, customer base, and more!

Seed start-up Insurance

- Few or no employees

- Often in co-working space

- In beta or just launched

Examples of basic Seed policies:

- General Liability Insurance

- Property Insurance

- Business Owners Policy

- Workers Compensation

Series A+ start-up Insurance

Examples of additional Series A+ policies:

- Directors & Officers (D&O)

- Employment Practices Liability (EPL)

- Fiduciary

- Keyman Insurance

Series B+ start-up Insurance

Examples of additional Series B+ policies:

- Product Liability

- Cyber Insurance

- International

- Intellectual Property

What Insurance Does a Startup Need?

There are essential business insurance coverages you may need to consider as a startup. Depending on the nature of your business and its structure, the types of imperative insurance may vary.

1: General Liability Insurance

When you sign a lease, it will probably require you to have basic general liability and property insurance to cover fire, flooding, third party damage, etc.

General Liability Will Offer Two Types of Protection:

General liability insurance — sometimes referred to as “slip and fall” insurance — is the most basic type of insurance and can protect your startup from small accidents and other on-premises mishaps. As a startup or small business, you will need to have some form of general liability insurance to safeguard your business and, by extension, your livelihood.

- Property Damage: Will provide your business with coverage if you or one of your employees damage someone else’s property. This includes the building or premises you are working on.

- Bodily Injury: Will provide your business with coverage if you or one of your employees injure or inadvertently harm the third party while working. This insurance type will take care of all medical care for the injured party and will also cover your legal fees if legal proceedings are sought against your company.

General liability insurance can also go beyond simple accidents and can include coverage for actions by your team outside of the office. It can also protect your startup if an accident occurs through the use of your products by customers.

When will you need it?

You first start your business. Policies are usually inexpensive for startups so general liability policies should not be considered optional.

Example of General Liability of Startup

If you are working with a client and something falls on them and seriously injures them, General Liability Insurance would cover the medical expenses and legal fees that result from that injury.

2: Property Insurance

Making Sure You Have Your Goods Covered

Property insurance will cover your startup’s physical assets in the event of loss or damage. A good policy will include property, such as buildings, equipment, furniture, computers, and other inventory as well as less-obvious protections such as virtual records. Your startup should be able to get a policy that covers all assets regardless of whether they are owned or have been leased. Coverage can also extend to personal property belonging to others that are in your business’ care.

This type of policy will provide for:

- The repair or replacement of your covered losses in the event of human-made disasters, such as theft and fire, and natural ones, such as earthquakes and hurricanes (Flood insurance requires a separate policy!)

- The replacement of covered physical assets in the event of loss or damage.

Many property insurance policies will also cover business interruption. For example, if, following an unexpected event your operations need to be suspended, this insurance would compensate for the loss of income and could assist you in fulfilling other financial obligations such as payroll.

When will you need it?

Start your business. Property insurance policy is also typically a requirement if your startup is carrying a loan from a bank or other financial institution. Furthermore, angel investors and business partners may require your startup to have property coverage.

Example of Property Insurance of Startup

If your startup property is burgled or vandalized, property insurance will cover the replacement of your included items.

Workers Compensation Insurance

In all 50 states, workers’ compensation insurance is mandatory after hiring the first employee. The cost is a percentage of payroll - the percentage depending on your industry sector.

Making Sure Your People Are Taken Care Of

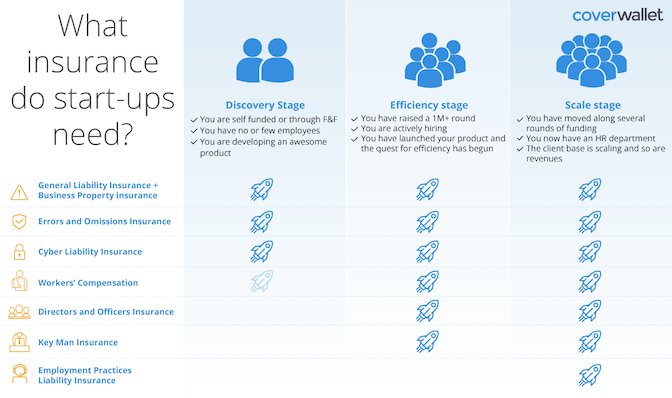

Infographic: Insurance for Startups

Workers Compensation can cover injuries to your employees while on the job, whether at the physical site of the job or elsewhere. Workers Compensation can also cover lost wages and medical treatment if an employee suffers a work-related injury or illness and is unable to work. It will also reimburse workers for lost wages until they can go back to work. As an employer, this is ideal, as it will protect you from employee lawsuits.

When will you need it?

Have employees on the company payroll. The laws differ from state to state, but usually, coverage to protect the welfare of your startup team is required by law. Regardless of your state’s laws, Workers Compensation Insurance is favorable to have as an employee-related lawsuit could harm your reputation and put your business at risk.

Example of Workers Compensation Insurance of Startup

A programmer at your startup develops carpal tunnel because of the amount of time she is spending at her computer writing code. Workers compensation can help cover her medical treatment and lost wages so you won’t have to.

How much does Startup Insurance Cost?

Insurance costs often depend on several different factors including location, claim history, business size, and type. You will be able to get an accurate approximation of cost by getting an insurance quote that pertains specifically to the needs and nature of your business.

Cyber Liability insurance

If you save client’s information (credit cards, SSNs, or simply names of people using your product), this policy can help you cover the cost of a data breach. For instance, most states require companies to notify customers of a data breach using certified mail.

Another insurance type to consider is Cyber Liability insurance. Cyber insurance for startups will cover you and your business against information security-related claims. The type of insurance you need for your startup will depend on what stage your business is in. Check out our handy infographic to understand what we mean:

Related content to Insurance for Startups

Frequently Asked Questions about: Startup Insurance

How long does it take to get insurance?

For most policies (general liability, professional liability, property and workers compensation), you can complete the whole process in a couple of minutes: submitting the information in our online form, getting a quote, making a credit card payment, and downloading a copy of your policy and certificate. It works from web or mobile, and even after hours.

Certain policies are geared for more complicated risks (e.g. Directors and Officers) and, as a result, will take longer to get a policy. Consequently, you can get a price indication after answering a few questions. If you want to purchase the option presented, an underwriter will need to review the application and verify the data. In some cases, you might have to submit additional documentation which results in the entire process taking 24 to 72 hours.

How can I know if I am buying the right Startup coverage?

If you have doubts, you can call us to discuss insurance options. Our licensed agents are ready to help, and speaking to them is completely free. You can speak to them for as much or as little as you want.

Is it cheaper to buy insurance from CoverStartups?

Insurance is regulated and our price is the same as the price you can get from somewhere else. Think of this as buying a plane ticket from Kayak, Orbitz or Expedia. The price is the same. But we offer convenience and speed to get a quote and bind in real time. 99% of other options you have to go over a 3 day analog process. Plus we offer unmatchable service after you buy insurance.

What are the payment options?

Believe it or not, most insurance companies don’t accept credit cards yet. But CoverWallet does. We allow you to pay via credit card or bank account. And you can pay in full or in monthly installments, whatever is more convenient.

How long does it take to receive a Certificate of Insurance (COI)?

As soon as you pay for your policy and bind it, you can download a Certificate of Insurance (COI). No need to wait for 24-48 hours like in the offline world.